There are not a lot of winners in this market. In fact, it is close to zero.

Seeing such wide-spread carnage makes me want to look for bargains AND for charts that have held up. I spent Friday morning stepping through the chart of every company in the S&P 500, the S&P 400 and the NASDAQ 100.

It was an ugly scene.

Only a few pockets are outperforming right now.

The first is utilities. But a bull market in utilities is anything but bullish overall. Utilities aren’t outperforming because of datacenter demand growth. Utilities are outperforming as a flight to safety.

The second major sector that is doing surprisingly well is another “boring” sector – insurance companies!

Source: Stockcharts.com

At first glance, I wasn’t sure why the insurance business was doing so well.

As it turns out, this is partly a flight to safety – after all everyone needs insurance even when things go bad.

But is there more to it than just that?

One BIG contributor, and one that surprised me, is the impact of artificial intelligence and LLMs—Large Language Models.

AI is transforming the way that the insurance business is done.

This is interesting because it is a secular move and because the gains from AI are all about efficiency, which means they translate directly to the bottom line.

AI is making it easier to acquire customers, price coverage accurately and assess loss more quickly.

The biggest benefit will confer to the companies with first-mover advantage, as they get improved margins and take share.

There is a WHOLE LOT of share to take – because the insurance business is so BIG.

According to Lemonade (LMND – NASDAQ) CEO Daniel Schreiber, the world spends more money on insurance than just about any other sector – automotive, cloud computing, even entire defense budgets don’t amount to what we spend on insurance.

If a company can get a leg up, the sky is the limit.

I’m going to take a look at what two VERY DIFFERENT insurance companies are doing with AI. And the difference it’s making to their top and bottom lines.

AIG – BACK FROM THE DEAD

Over the past decade American International Group (AIG – NYSE) has undergone a remarkable transformation.

This was a company that was a corpse at the end of the Great Financial Crisis. For years after it was a walking dead.

When CEO Peter Zaffino took over in 2017, AIG faced significant challenges. They had “a lack of underwriting discipline, high expense ratios, and inconsistent data management”.

Zaffino described the situation as “sink or swim”.

Swim they did. AIG has since re-positioned itself as a leader in the global insurance industry.

Maybe because they were in such dire straits, AIG took the chance on modernizing their business.

The company streamlined operations, eliminated 1,200 legacy applications, modernized data infrastructure, and moved 80% of its systems to the cloud.

Integrating AI was a big contributor and it has driven impressive results.

REAL USE-CASES FOR AI

When it comes right down to it, insurance is paperwork. If you can get that paperwork done faster, you are already a step ahead.

Enter Palantir (PLTR – NASDAQ) and Anthropic’s Claude AI.

I’ve always wondered what Palantir does. I’ve now figured out at least one thing they do – develop and power AIG’s AI underwriting models.

Along with Claude, Palantir makes that paperwork go much, MUCH faster.

AIG uses AI to find the data and fill out the forms. And it does it fast.

This has always been possible to some extent, but with LLMs it is far less limited. AI does not care the format of that data. A Word document, a PDF, a picture, or even social media, LLMs can grab and evaluate the data in seconds.

This all brings the underwriter to the point of decision much faster. During the AIG Investor Day Zaffino said that tasks that previously took weeks can now be completed in hours.

A second way AI helps is with prioritizing the time of the underwriter.

AIG uses the reasoning power of AI to help determine which policies will be the biggest bang for the buck.

That ensures that underwriters are focusing their time effectively. And that the policies written are driving the highest returns.

Source: AIG Investor Day Presentation

Finally, AI helps drive better pricing.

AI’s ability to consider massive amounts of data, connect the dots to historical comparisons, and “reason” likely outcomes means that AIG can price their insurance more accurately.

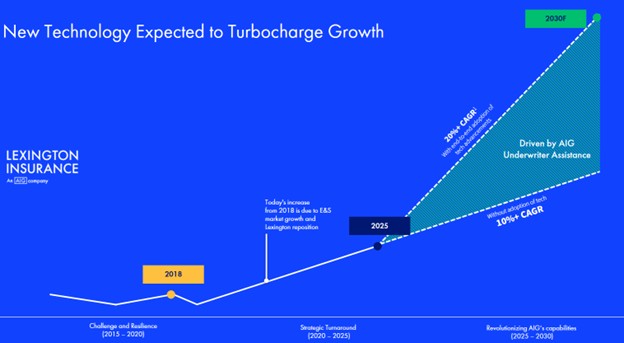

Again at their Investor Day, Zaffino stepped through the case study of one of their businesses, their Lexington Insurance line.

Lexington is a surplus insurer, which means it insures the “extra” risk that another insurer might want to offload.

To get to the punchline, Zaffino said that AI has helped double the CAGR compared to what it would be without tech adoption. Which amounts to a massive inflection in the business.

Source: AIG Investor Day Presentation

Multiply that across all of AIG’s insurance lines, AI is helping produce some impressive numbers:

• 20% compound annual earnings growth

• Return on equity (ROE) of 10%+ in 2025, and 10%-13% by 2027.

• Expense reduction dropping 10-15% and their expense ratio dropping to 30% – a REALLY efficient number

So that’s AIG, using AI to drive profits. My second example is using AI to a different end – to drive market share and growth.

LEMONADE – BUILT ON AI

While AIG has reshaped a centuries old business on AI, Lemonade has done the opposite, building their AI-based insurance business from the ground up.

Lemonade’s proposition is simple: a built-from-scratch AI will “quantify risk and collapse costs in a way that no other structure” will.

Lemonade LOVES to compare themselves to legacy insurers. They point out that GEICO, one of the largest insurers and one that has been around for 90+ years, operates over 600 legacy systems and most of them don’t talk to one another.

Lemonade is the opposite. Everything is connected, everything is talking and wherever it can everything is automated by AI.

In their last Investor Day Lemonade took investors through the case-study of their most recent insurance line – auto insurance.

Lemonade got into auto insurance when they bought the pay-per-mile insurer Metromile in 2022. Today auto insurance makes up 13% of their in-force premium.

Source: Lemonade Investor Day

They’ve grown their auto business, and all their lines, by using AI to drive more precision and more efficiency. That translates into market share gains and lower prices for drivers.

It all comes down to pricing risk more accurately. Which can be done through what is called “disaggregation”.

What is disaggregation? Insurance companies generalize a lot. Age, gender, income strata – they are always trying to put you in a bucket. That’s aggregation.

Lemonade is trying to take you out of the bucket – disaggregate you. With their car insurance product, they use telematics and AI to evaluate you as a driver. Which allows them to better pinpoint your specific risk.

At their Investor Day Lemonade used the example of “Jack”.

Jack is a young driver that comes to Lemonade looking for auto insurance. Lemonade needs to decide what price Jack should get.

How do they do that?

What Lemonade doesn’t do is generalize based on Jack’s age or other demographic.

Instead, Lemonade monitors just how good of a driver Jack is – through his smartphone.

They use the phone GPS, gyroscope, motion data and acceleration detection to evaluate Jack. Their AI model digests the data and comes up with an assessment.

As a result, if Jack is a good driver, he gets a better rate.

Source: Lemonade Investor Day

No surprise that Lemonade is targeting a younger demographic. It’s a strategy that makes sense because in the traditional insurance model of aggregation, younger drivers pay more.

Source: Lemonade Investor Day Presentation

But by looking at Jack individually, Jack benefits with lower priced insurance. Lemonade benefits by adding a customer. A win-win.

But that’s just one piece of the AI journey. As with AIG, using AI to do the legwork brings Lemonade’s data acquisition costs down a lot.

More importantly, because Lemonade isn’t hiring underwriters to do the work, those costs don’t need to scale as the top line grows. Which is why Lemonade has been able to grow their business for 5 years without a corresponding increase in operating expense.

Source: Lemonade Investor Day

Also like AIG, AI is helping Lemonade decide if Jack is worth their time.

At their Investor Day Schreiber talked about their LTV model. Now in its 11th generation, this customer screening platform is comprised out of 50 different learning models and uses more than 3.6 billion data points.

Source: Lemonade Investor Day

Before Lemonade ever reached out to Jack, their AI tools made sure that the returns on Jack were worth pursuing.

The success of that model is in their results, as Lemonade has grown its customer base efficiently for the last 5 years.

Source: Lemonade Investor Day

Finally, Lemonade doesn’t stop evaluating Jack after the policy is signed.

Lemonade continues to monitor Jack. That helps evaluate Jack for the next period and helps tune the model to be even more accurate in the future.

Source: Lemonade Investor Day

The entire process is fused by AI and is also self-reinforcing. Which is what lets Lemonade confidently say they expect their growth rate to increase in coming years (more on that shortly).

SOW THE SEEDS OF AI,

REAP THE REWARDS

I’ve looked at two insurers from COMPLETELY different ends of the spectrum. Both using AI to upend the industry. Both are using it to different ends.

AIG is using their gains to become more profitable. In turn, AIG is using those earnings to deliver shareholder returns.

AIG has aggressively returned capital to shareholders. Since 2019, the company has bought back nearly 300 million shares (33% of outstanding shares) and steadily increased their dividend.

Source: AIG Investor Day

In 2025, AIG plans to repurchase $5-$6 billion more. (!!!)

Lemonade’s focus is growth.

Accelerating growth is no small feat for a company as large as Lemonade. Yet at their Investor Day, Schreiber said that “25 will grow faster than ’24, ’26 will grow faster than ’25… we [expect to] grow into that 30% CAGR”

It comes at the expense of profitability. Lemonade bluntly admits they are pricing their insurance cheaply to gain market share.

But that doesn’t mean they are burning cash. EBITDA margins have improved for 5 years straight. They expect to be EBITDA profitable in 2026.

Their adjusted free-cash flow, which includes a very unique model for marketing spend, is already positive.

Source: Lemonade Investor Day

KEEP IT IN YOUR BACK POCKET

Look, there is A LOT to consider when buying an insurance business. A lot of puts and takes.

A big risk today is what an insurer can invest their cash in. With Treasury yields coming down, lower investment income could become a headwind for earnings.

A second risk is inflation. If tariffs drive prices higher, insurance company profits suffer until their policy premiums catch up.

Lots to consider! My focus is purposely narrow: the impact of AI. What I hope to get across are two important points.

First, there are REAL-WORLD use cases for AI that are being rolled out today. These use-cases are driving better results.

Second, companies that adopt these tools first get a leg up on the competition. Which translates into better margins and more growth.

Finally, let me end with one last take-away.

As investors, we are being re-acquainted with risk this last week.

The insurance business, on the other hand, is always pricing risk. It is what the business does!

Taken together, maybe it is not so surprising that the sector is outperformin

THE ONLY COMPANY TO REVERSE LATE STAGE LIVER DISEASE WHAT’S THAT WORTH?")

")

THE ONLY COMPANY TO REVERSE LATE STAGE LIVER DISEASE WHAT’S THAT WORTH?")

")

AND MAKO MINING (MKO – TSXv)BOUGHT CHEAP AND SEE THEM NOW!")