The Largest “Ethical” Cobalt Explorer in the World is Created

The #1 cobalt explorer in the world is being formed now with a proposal for a 3 way merger that would unite one of the leading cobalt camps outside the Congo.

This is what institutional buyers have been waiting for to get direct exposure to cobalt, a major metal in batteries for electric vehicles (EVs) and the fast growing battery storage market.

If this proposal becomes reality, the combined assets of First Cobalt (FCC-TSXv), Cobalt One (CO1:ASX) and CobalTech (CSL-TSXv) will bring together more than 10,000 hectares of prospective cobalt-silver properties, 16 historic mining operations, a mill and a refinery with 40 acres of fully permitted property just outside the town of Cobalt Ontario, near the Quebec border. The deal is still a Letter Of Intent, but Mell is confident it will get approved by shareholders. It just makes too much sense.

“It becomes a good (public) vehicle,” says First Cobalt Trent Mell, who will remain CEO, and the merged name will stay First Cobalt.

The permitted mill and refinery is key. With it, Mell says there is a possibility of near term production.

“We have the mill equipment already there,” Mell says. “The reality is that within a year we could be taking stockpiled material from historic mines; putting it through our mill facility and be shipping concentrate direct to China. So really, there are 12-24 month cash flow scenarios.”

This is exactly what institutional investors would want to see. Mell believes the new First Cobalt will have a market cap of roughly $100 million—enough to attract institutional interest. He says there are over 50 other cobalt explorers listed on Canadian exchanges, with all of them having market caps of $30 million or less—Big Money institutions can’t buy those stocks.

Cobalt prices hit a new 9 year high this week—over USD$26.50 per pound. Hedge funds and ETFs have already started hoarding the metal, anticipating a supply crunch.

The merged entity will also have two of the most successful mining entrepreneurs in North America on the board—Paul Matysek and Robert (Bob) Cross. Matysek is the most successful energy metal management man in the world, having built and sold:

- Energy Metals to SXR Uranium in 2007 for $1.8 billion

- Lithium One to Galaxy Resources in 2012 for $112 million

He also built and sold Potash One to Germany’s K + S for $434 million in 2012.

Cross is a Harvard MBA with a long track record of creating shareholder value in resources:

1) Bought control of Northern Orion in 2003 at $15 million market cap & sold it to Yamana Gold in 2007 for $1.4 billion

2) Co-founded Bankers Petroleum in 2004, became Chairman, reached market cap of over $2Billion in 2011.

3) Co-Founded B2Gold in 2007, still Chairman, now $3.7 billion market cap, producing almost 1mm ounces/year

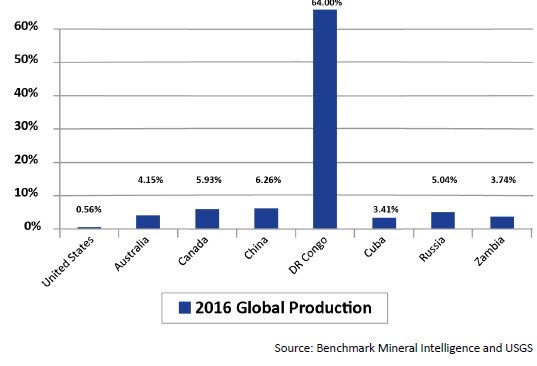

I wrote in an earlier article that cobalt supply is much precarious than any other metal in the EV supply chain. And that should make the price increases be potentially even higher than the more abundant lithium—and the chart above shows that.

But getting a large supply of ethical cobalt is not easy. Here is the problem I wrote about only a month ago:

“Over 60% of the world’s cobalt comes from the Democratic Republic of Congo. Three-quarters comes as a by-product from copper or nickel mines where production is only as secure as the host country.

“The other 25% of Congo’s cobalt is mined “artisanally”, which means it comes from small mines that are often very unsafe.

“Thousands of under-age workers are used, sent down into hand-dug tunnels and shafts that can and do collapse—to pull out bags of rock. Several media stories have exposed this practice.

“This is starting to change. In early March, Apple stopped buying cobalt mined by hand in the Congo, saying all small mine suppliers will have to meet its workplace standards. Other companies have made similar noises.”

The new, larger First Cobalt has the potential to be the first company to fill that gap, and as the Market recognizes that the stock will get A First Mover Advantage—a premium valuation.

Mell says the investment community should not expect miracles in the short term, but the potential for quick cash flow is real:

“The Big Prize–a buyout at a premium valuation–is in the 5-7 (year time frame). But we are motivated to find some short term cash flow and limit the burn and dilution. With everything we’ve got we can ease into production and scale up over time.”