The rally in WTI oil prices that began at $42 per barrel in June 2017 and touched $77 in June 2018 (an 83% increase in a year) has fizzled in recent months.

If you were wondering what took the air out of the oil market oil trading superstar Pierre Andurand suggests that you look towards China.

I think he is onto something…..and that you shouldn’t be giving up on your oil stocks just yet. In fact it is likely time to be buying more.

Andurand recently tweeted:

The weak oil physical market is not only due to more OPEC oil on the water. It is mainly due to China destocking. Their low imports are not sustainable. They have been very low for 3 months. Their imports could go back up 2mbd any time now.

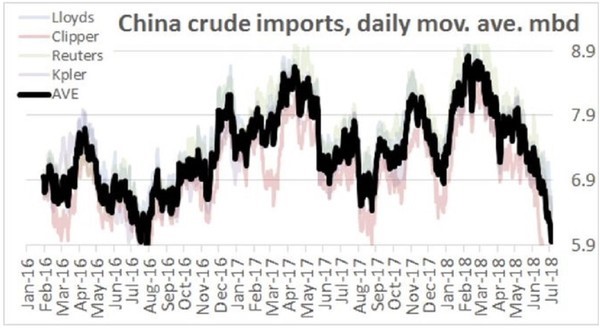

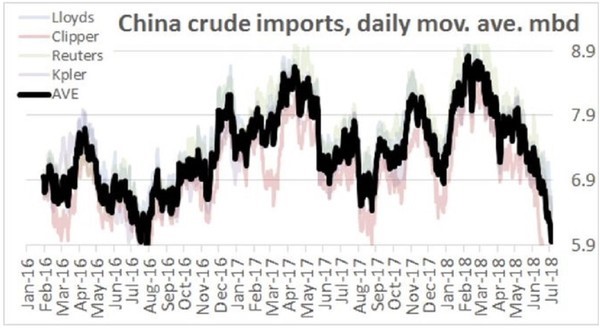

Andurand then also tweeted the following graphic. It provides estimates of China oil imports from several reputable sources:

It’s east to see what he is talking about. Chinese imports have clearly fallen hard since May—down from 7.9 million bopd (barrels of oil per day) to just 5.9 million bopd.

A two million barrel per day drop is certainly more than enough to suck the momentum out of oil prices.

In his tweet Andurand notes that he doesn’t believe that this drop is sustainable. What he doesn’t provide is the reason why he believes that.

I don’t doubt that he is right, but opinion without reasoning isn’t of much use to us — so let’s try and fill in that blank.

China Imports Are Down – Chinese Teapots Are The Reason Why

China has two classes of refineries.

The majority (roughly 70 percent) of China’s refining capacity rests with the state-owned oil majors — Sinopec, CNOOC, Sinochem and PetroChina.

The Chinese government is fully behind those companies.

The rest of the refining capacity (the other 30 percent) is controlled by independent operators. These refiners are often called “teapots” both because of their small size relative to the state owned giants and because of their ramshackle appearances.

On average the teapot refiners have a refining capacity of 70,000 barrels of oil per day. The range is from as low as 20,000 barrels per day up to 100,000 barrels per day.

The Chinese government doesn’t give a hoot about this motley crew. The teapots are competition for the state-owned operations.

Prior to 2016 the Chinese government restricted the teapots from directly importing crude oil — the essential refining feedstock in their business. Instead the teapots were forced to purchase their oil from Chinese state-owned oil companies at a price above market rates.

That obviously took a chunk out of profits. The Chinese government was ok with that.

Then in 2016 the Chinese government had a change of heart and decided to grant the teapots oil import licenses. A sudden act of kindness? No, this was an effort to help compensate for production shortfalls from state-owned oilfields.

China needed more oil and granting these import licenses helped secure it.

With lower input prices–avoiding the state mark-up on oil purchases—the teapot refining profitability soared. The good times rolled and the keep rolling for a couple of years.

On March 1, 2018 those good times ended.

You see, prior to being allowed to import oil, the teapots had squeaked out a profitable existence largely thanks to a tax loophole. That loophole had allowed them to declare fuels such as diesel and gasoline as “other oil products” and thereby avoid a consumption tax.

The Chinese government allowed this because some refining capacity on top of the state-owned amount was needed. This loophole remaining open allowed the teapots to survive.

With the teapots now not just surviving, but thriving, the Chinese government had no reason to keep the loophole open.

As of March 1, 2018 that loophole closed—and the consumption tax now in place is severe—$38 per barrel on gasoline and $29 on diesel.

That will take a bite out of income.

Not only have the good times ended but many of the teapots are struggling just to survive. With cash flows crushed, the teapots have had to greatly reduce the size of their refining activities—and therefore are purchasing/importing a lot less oil.

Some of the teapots even closed for maintenance during May and June rather than operate at a loss. Those refineries aren’t importing any oil. It is expected that many of them won’t ever reopen under these conditions.

Now take a look at Andurand’s graph again (below).

The consumption tax was enacted March 1, 2018 — the decline in Chinese oil imports starts immediately thereafter.

I think we have found the “why” that we were looking for.

The Teapot Refineries Have Slowed –

Chinese/Asian Consumption Hasn’t

The Chinese teapot refineries are really the middle man.

They refine crude oil into the finished products that are consumed in China and in various other parts of Asia.

While the teapot demand for importing crude may never rebound—somebody has to supply those finished products. Those consumers don’t care who refines the gasoline or diesel they are using.

The state-owned refineries will pick up some of the slack–their utilization rates will increase. The Chinese government will like that. The best-run, most efficient teapots will pick up more of it. The teapot sector will consolidate and the most profitable companies will thrive, albeit with tighter margins.

Maybe some refineries outside of China will pick up some of the slack — I don’t know for sure.

What I do know is that demand for oil in China and the rest of Asia hasn’t changed much.

Andurand is right about the fact that the reduction in Chinese imports is not sustainable and will rebound.

Because China is such a big part of the global oil market, this is a big deal. What would another two million barrels a day of oil demand for 7 months—to restock the Chinese oil cupboard—due to oil prices? I think a lot.

The Market just doesn’t know when that will happen.

EDITORS NOTE: I think The Bakken is once again one of the most profitable oil plays in North America—you only have to look at the stock runs of Whiting (WLL-NYSE) and Continental (CLR-NYSE) to see that. But the Market is completely missing this $2 stock as it almost doubles production this year and will almost double it again next year. I’m convinced shareholders will enjoy an incredible autumn season with this company… I give you the full report, risk-free, by clicking HERE.

VS. TECHNICALS (GOOD)")