Apache’s new High Alpine discovery on the SW edges of the Permian Basin is one of the three most important inflection points in the North American energy market in the last decade.

(The other two are the rise of the oily Bakken play in North Dakota and the gassy Marcellus play in Pennsylvania.)

The huge size of the new High Alpine discovery, plus Resolute Energy’s game changing drill results giving them 1 year paybacks at $45/b

WTI—means the entire Delaware basin, almost half the Permian—is now economic right now, at $40-$45 oil.

This is a huge play that will steal capital from other US plays.

To me, it means a clear hierarchy of the horizontal oil plays in the United States has emerged. There are now Tier 1 plays that make money today while the rest don’t; they’re Tier 2.

Three of the Top Four are sub-basins of The Permian, and the other is the STACK, or Woodford, oil play in Oklahoma.

These are the only two large plays that are economic in the $40-$50/barrel range that WTI has been trading in—and that’s where the Market

now expects it to be for the next 6-9 months.

It really makes the rest of the US plays—second rate.

That sounds harsh, but in this range bound oil pricing–unless some kind of innovation comes along for oily plays like The Bakken—this once leading play will quickly become an afterthought for producers, investors and statistics keepers.

There is no reason to allocated capital to the Bakken today because it is a money losing proposition. Even at higher oil prices it will make significantly less money that the Tier 1 plays.

I’m not saying that these Tier 1 plays enjoy spectacular economics—but they are solid. That is not something anyone ever expected from a horizontal oil play at $45 WTI.

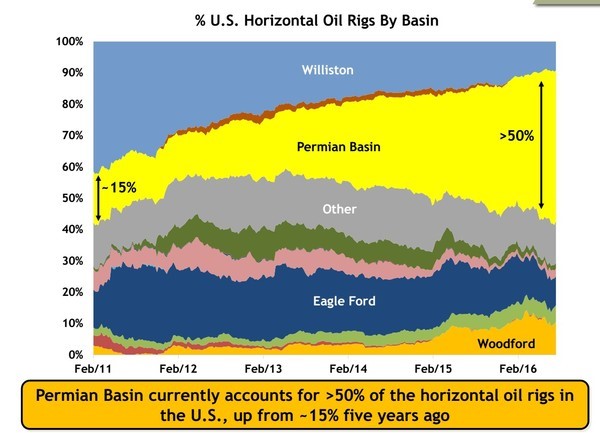

Follow The Horizontal Rig Count

Every CEO and company spokesperson is going to tell you great things about his or her company’s assets no matter what the truth is.

You can’t blame them for that.

Imagine the shareholder outcry if the CEO of the producer they owned was going around telling everyone how terrible the company’s drilling opportunities actually are.

Instead of using your ears, use your eyes.

Watch what the industry is doing.

Source: Pioneer Resources Corporate Presentation

The horizontal rig count chart above paints a very clear picture.

Money is rushing into the Top Tier plays and out of the others.

Follow the money. Or in this case follow the money that is being spent on drilling.

By doing so we can draw a couple of simple conclusions.

Permian Basin and Woodford = Economics Worth Drilling Today

Bakken and Eagle Ford = Economics Not Worth Drilling Today

If every company in the Bakken had the option to drill in the Permian or Woodford I’m sure the rig count transfer would be even more significant.

Owning the low cost producers is the best way to go for long term energy investors. Not only can the low cost producers withstand lower commodity prices, they also generate much higher returns on capital invested when commodity prices are higher.

The top tier horizontal oil plays are the ones that investors should want to own.

Low cost wins…always.

In The Top Tier $40 WTI Works – $50 WTI Looks Really Good

The exact economics for all these horizontal oil plays is always a moving target. Service costs for drilling and fracking will move around, depending on how desperate the service companies are for business. Plus the big thing is that technologies and techniques are still evolving every month.

What we do know for certain is that the Top Tier plays have superior economics at all oil prices.. We also have a pretty good idea what the economics look like today.

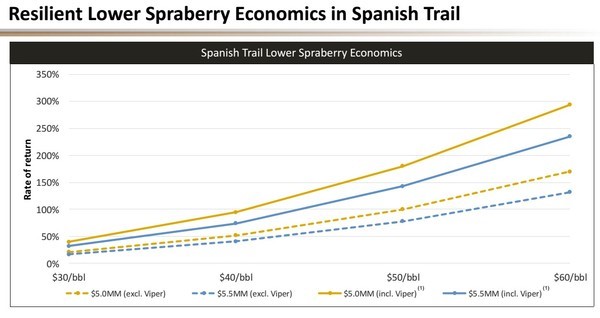

Pioneer Resources is by far the most active Spraberry/Wolfcamp operator in the Midland Basin, which is the eastern side of The Permian in SW Texas. Everyone now knows the Midland Basin is one of the top horizontal oil plays.

Source: Pioneer Resources Corporate Presentation

The current type curve Pioneer presents shows rates of return of up to 100% for Lower Spraberry wells at $40 WTI. At $50 WTI the returns reach as high as 175%. The wells are worth drilling at $40 and are great investments at $50.

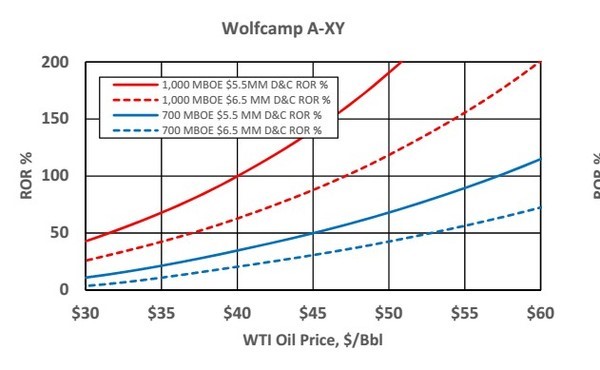

The Delaware Basin is now—thanks to Resolute Energy’s game changing drill results this summer—clearly the Permian’s second top tier horizontal oil play. The Delaware has come into focus this year with a number of large transactions taking place (at rich prices) and eye-opening drilling results emerging.

Matador Resources is a significant Delaware Basin operator and is showing Wolfcamp rates of return that are very similar to Pioneer’s Spraberry wells.

Source: Matador Corporate Presentation

Again at $40 WTI these wells are worth drilling. At $50 companies are looking at rates of return that will allow for significant growth.

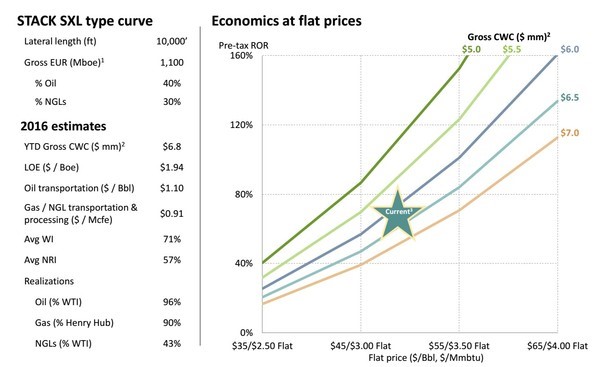

The Woodford or STACK is the third top tier horizontal oil play. The STACK isn’t in Texas but rather Oklahoma.

Source: OGFG.com

The play itself is different than the Permian plays in that only 40% of production is oil. A high natural gas liquid content (30% of production) is a big part of what makes the economics here so compelling.

Source: Newfield Exploration Corporate Presentation

At current oil and gas prices these STACK wells generate rates of return over 50% and are expected to get closer to 100% as drilling efficiencies continue to improve. Again, solid rates of return at a very low commodity prices.

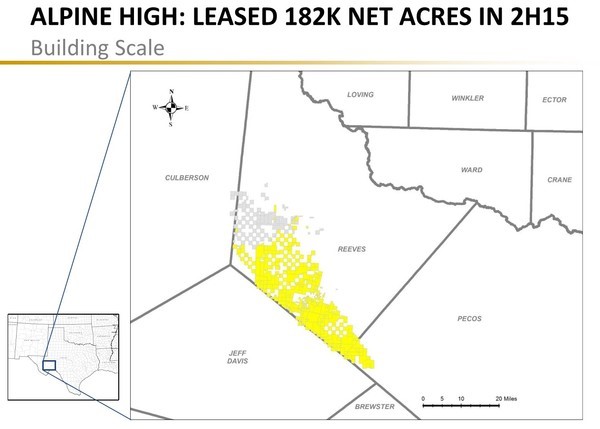

The fourth top tier horizontal oil play is the new kid on the block. It is also in the Permian and is along the southern boundary of the Delaware Basin.

Apache just let the cat out of the bag on this one, stunning investors with a massive acreage position in what it calls the Alpine High. Apache accumulated this acreage for only $1,300 per acre a mere fraction of the $30,000 per acre prices land elsewhere in the Permian has been going for.

Source: Apache Corporate Presentation

The industry had overlooked this corner of the Permian because of what it thought was “challenging” geology. Apache has gone in, cracked the code and built up a huge land base.

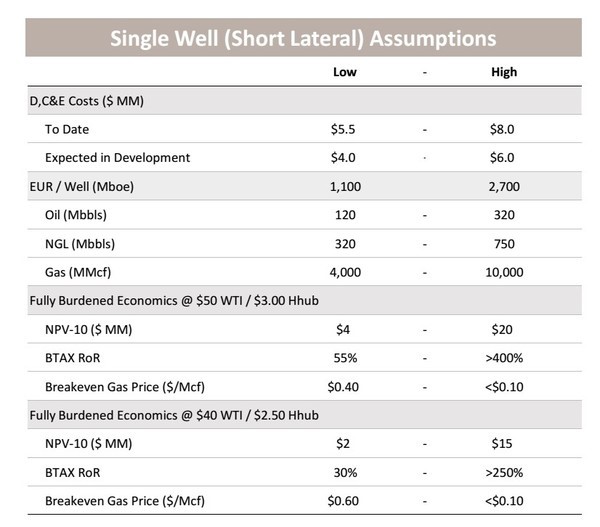

The type curve that Apache is modelling is showing solid rates of return at $40 WTI and outstanding numbers at $50 WTI.

Source: Apache Corporate Presentation

With a ramped up drilling program you can bet the well costs will come down further and production rates improve.

For all of these Top Tier plays $40 WTI works and $50 works really well.

Core Bakken Operators Who Are Shutting It Down

To truly appreciate how much of a backseat the Bakken now finds itself in we need look no further than some of the regions dominant producers.

In my next article I’ll dig deeper into Bakken heavyweights Continental Resources and EOG Resources to see what they are saying…..and more importantly doing with their Bakken assets.

Keith

Editor’s Note: All the Big Boys have moved into the Delaware Basin because of the incredible economics. But I recently found one Micro Cap in the play with Large Cap management. I expect TWO Big CAtalysts in the next 60 days. The name and symbol are right HERE

VS. TECHNICALS (GOOD)")