Low prices, high discounts and high condensate prices are conspiring to make this The Week From Hell for Canadian heavy oil producers. Heavy oil prices are now at the bottom of the barrel.

And not to sound like a traitor, but there is a very simple way for investors to profit from this, which I’ll explain below.

All energy investors know the oil price has been hammered, though few realize that only a few North American producers—basically Texas—actually gets WTI pricing. Almost every other producer on the continent gets a discount to WTI—which is often just the price to transport the oil to Cushing Oklahoma. (So it’s really worse than you think out there.)

The industry word for discounts is “differential” or diffs. And the diffs for Canadian heavy oil—Western Canada Select or WCS–are huge now, due to refinery shutdowns, pipeline closures and just plain old more supply. Higher “diffs” = lower prices.

Source: ARC Financial Energy Charts Aug 18 2015

Heavy differentials were arguably tighter/lower than they should have been in June and July as several forest fires in western Canada took as much as 230,000 b/d of heavy oil production off line for several weeks. Reduced supply = higher prices; simple economics.

But this was a temporary situation and The Street knew differentials would “normalize” when production came back on line.

But putting the flames out coincided with Imperial Oil’s (IMO-TSX/NYSE) Kearl project starting Phase 2 production in late June. It will likely take up to a year to add the full 110,000 b/d–but by the end of August it’s estimated that at least a quarter of that volume will be on production.

And that production number is climbing daily. And there’s more supply coming.

ConocoPhilips’s (COP-NYSE) Surmont Phase 2 and Husky Energy Inc.’s (HSE-TSX)Sunrise Phase 1 both of which started the steaming process in the past couple of months and could see incremental production coming on before year end.

The massive scale of these projects more than offset declines in the conventional heavy production. It won’t be until you see one of these major projects shut in that you will see heavy production start to flatten or decline.

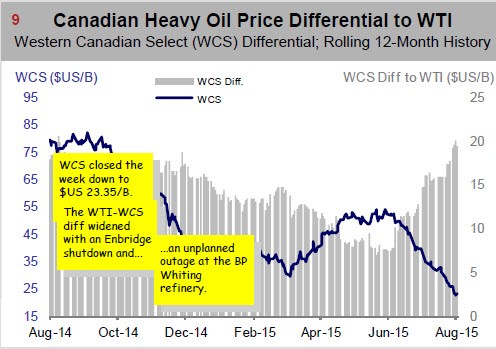

Now…queue the refinery shutdowns. On August 8th heavy oil producers suffered a big blow with an unplanned outage at BP’s Whiting refinery near Chicago. This refinery,which runs almost 10% of all Canadian heavy crude production, lost 240,000 barrels of its refining capacity of 413,000 barrels a day after a malfunction.

In an already illiquid market for Canadian heavy oil, losing a primary consumer of your supply can be devastating to prices–and it was. Almost overnight the “diff” for WCS widened US$2-$3 per barrel. No one knows when this capacity is coming back online, casting a further pall over the market.

The week from hell continued for heavy producers with Enbridge (ENB-NYSE/TSX) suffering a leak on its Spearhead pipeline on August 11th resulting in the pipeline shutting down, adding another US$2-3/bbl onto the WCS “diff”.

Spearhead is one of the primary means for Canadian heavy crude to get to alternative markets—like the Gulf Coast. After BP Whiting went down, losing access to the main alternative market was a serious blow. Granted, the Spearhead Pipeline shut down only lasted two days, by then the damage was already done.

And to top it all off, condensate pricing is high again. In the ground, condensate is a gas that condenses on its way up the well bore and is produced as a very light (50 API) oil. Heavy oil producers use it to dilute/blend with their gooey product so it will flow in a pipeline. As a rough rule of thumb, producers use 70% bitumen and 30% condensate to get their oil into a pipeline.

This was made even worse when the Alliance Pipeline shut down for six days because sour gas mistakenly got into the system. This 3700 km pipeline sends 1.6 billion cubic feet of gas from Alberta to the Chicago area—it’s one of Canada’s biggest export pipelines.

The shut down of Alliance forced several condensate producers to curtail all production for six days. Seven Generations Energy (VII-TSX) alone produces over 20,000 bbls/day of condensate which can dilute almost 50,000 bbls/day of bitumen production (assuming a 70% bitumen/30% diluent blend ratio).

As heavy differentials widen and condensate strengthens—this lowers profits for heavy oil producers. Since July, the higher differentials and higher condensate price has shaved just over $5 per barrel profit for producers. That doesn’t even include the lower oil prices from which those diffs, or discounts, are based!

So…heavy oil production is increasing. The industry is its own worst enemy there. This increases condensate prices—and then supply got even tighter with the pipeline shutdown. Unplanned refinery maintenance in their major market.

While some of these issues are temporary, a couple are not. The longer term realities are:

1. oilsands production will continue to increase for another 3-4 years

2. refineries shutdown every fall and spring to do maintenance, reducing demand

3. in winter, North America uses less heavy oil

As investors, we don’t make the rules. We just owe it to our families to profit from them. There is one stock that profits from all of this. Since I alerted subscribers to it earlier this year, it’s up almost 20%. They increased their dividend last quarter. I expect them to increase it again this quarter.

I’m definitely saying a prayer for Canadian heavy oil producers. They need it. But to profit from it right now—CLICK HERE