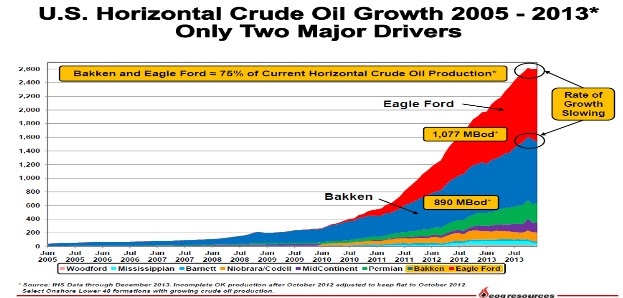

If you are looking for a reason to get bullish on future oil prices look no further. The chart below is one of the most bullish charts in the energy patch today.

This chart tells us two critical things.

First, it tells us that the horizontal oil boom is due almost entirely to only two plays, the Bakken and the Eagle Ford. Second, it tells us that production growth in these two plays is flattening significantly.

And the news gets worse (or better if you are long oil), because according to the most informed horizontal driller in the United States, there is no “next” big horizontal play waiting in the wings to follow the Bakken and Eagle Ford.

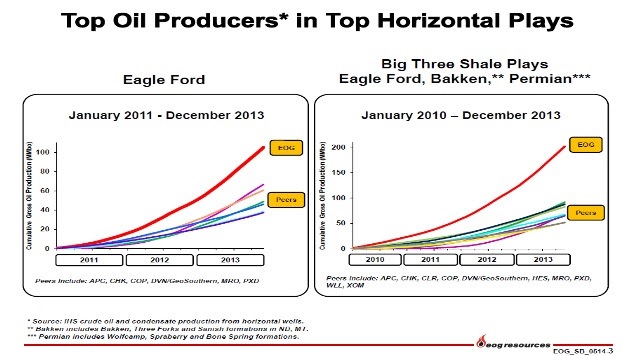

EOG Resources has perhaps the best visibility on where horizontal oil and WTI prices are going. EOG is the largest horizontal oil producer in the United States (and therefore the world) by a considerable margin.

EOG produces twice as much oil from horizontal wells than its nearest competitor. This is the foremost voice on American horizontal oil production.

EOG’s CEO and Chairman Bill Thomas recently spoke at the Sanford C Bernstein Strategic Decisions Conference and made very clear that his company is very bullish on oil prices.

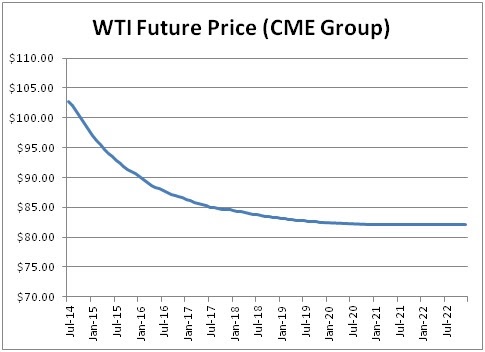

Thomas was specifically asked at the conference if he was concerned about the lower prices that the futures market was predicting for oil. His response was that he believes that the futures market is mistaken and that the steeply steeped backwardation is inaccurate.

Source of graph data: CME Group

The front month prices of West Texas Intermediate oil futures is now, and has been in a very steep state of backwardation. Backwardation is where the prices of contracts with later delivery dates are trading well below the near term contract price.

Where today WTI is selling for over $100, looking forward to 2017 and beyond the market seems to think that the price of oil will be closer to $80.

I can’t ever be sure why the market does what it does. Most people think it’s because while geopolitical events are supporting the near term price of crude, the surging supply of American oil production will cause it to drop in the longer term.

What EOG and Thomas believe is that despite the incredible rate of growth in US oil production, pure crude oil horizontal plays are actually very rare and becoming harder (not easier) to find.

Thomas notes that EOG has scoured the country looking for a third major horizontal oil play to follow the Bakken and Eagle Ford but the search has come up empty.

There are other, smaller high quality oil plays but there is nothing in the pipeline that is close in size to the main two. Together the Bakken and Eagle Ford account for 75% of horizontal oil production in the United States.

There’s no Third Act here, and production growth in the Bakken and Eagle Ford is already slowing.

The Bakken and Eagle Ford are so special not just because they’re big; they’re also simple. They’re like flat layer cakes that go for tens of miles, and there are no surprises; you know where the oil is and how to turn the well to go horizontal in every well.

Now look at the Monterey formation in California. It’s potentially big, but it sure isn’t simple.

In 2010 the EIA (Energy Information Agency) announced that the Monterey contained almost 14 billion barrels of “technically recoverable” oil. At that figure the Monterey made up 60% of the recoverable shale oil in the United States.

This spring, the EIA recently reduced its estimate of recoverable oil in the Monterey by a whopping 96%…..down to only 600 million barrels. The reason? It’s not a layer cake, it has been tectonically rolled over a few times and oil is in tough to get at small chunks.

Now, IMHO, there are two Brutal Facts that could kill EOG’s Beautiful Theory (and for all energy investors, it’s Beautifully Bullish Theory).

One is the Permian Basin in west Texas. It’s big and simple; the right makeup for horizontal production capability.

But Thomas contends the Permian is not a pure crude oil play. The Permian is a “combo” play–meaning that it has lots of natural gas, and natural gas liquids, but not nearly the quantity of oil that the Bakken and Eagle Ford have.

EOG’s Thomas addressed the Permian specifically at the Bernstein conference by noting “that while the Permian has a big boe (barrel of oil equivalent) count, the play is heavy on the “e’s” and not so much on the “o’s”…….”.

Gotta say, I’m not convinced on his Permian argument. But I think his overall point is valid. The core of the Eagle Ford and Bakken are being drilled now and everyone is extrapolating to a huge extent.

The second Brutal Fact is something that EOG is doing itself, and very well—increasing recoveries. Producers are learning how to get more and more oil out of wells, and they’re putting down more wells every square mile than ever before. That doesn’t kill the theory, but it could sure delay it by a few years.

The company continues to innovate in both the Bakken and Eagle Ford and increasing both the quantity of oil that can be recovered and the profitability of each produced barrel.

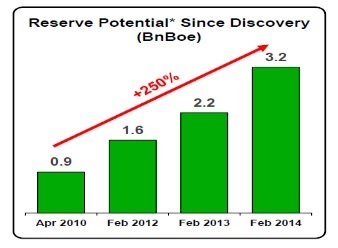

Since entering the Eagle Ford in 2010 EOG has increased its internal estimates of oil reserves in the play from 900 million barrels to a staggering 3.2 billion barrels.

That increase has been created through trial and error. EOG has worked to figure out the optimal number of wells to drill on the land and where to place them.

The company has also increased productivity of each well by perfecting drilling and completion techniques that have allowed for the amount of oil recovered per well to be increased.

And EOG isn’t done making both the Eagle Ford and Bakken bigger. The next step is going to come through enhanced oil recovery which is common to the oil industry but not to horizontal production. Through the application of water or natural gas flooding it is likely that recovery factors in these plays will again rise significantly.

For investors, the takeaway is that yes the horizontal boom is real and will continue, but the rate of production growth is going to slow and there isn’t another Bakken or Eagle Ford in the on-deck circle.

That should be long term bullish for oil prices and may eventually show the current futures curve to be significantly too low.

VS. TECHNICALS (GOOD)")